Macro Report August 2023

Internacional

Em julho as bolsas ao redor do mundo tiveram performance positiva meio a divulgação de dados de crescimento e de inflação que pintaram um cenário mais otimista para a economia americana.

O comitê de política monetária dos EUA elevou a taxa de juros básica para o intervalo de 5,25% - 5,50% a.a., sinalizando que novas altas podem ocorrer a depender dos dados de inflação e do mercado de trabalho. A boa notícia é que a criação de empregos caiu pelo segundo mês consecutivo, e a inflação atingiu a menor alta em dois anos (3,0%). Também houve divulgação do PIB americano, que cresceu 2,4% no 2º trimestre de 2023, impulsionado pelo setor de serviços, o que contribuiu para uma maior expectativa de soft landing entre os investidores.

Na Zona do Euro, o Banco Central Europeu elevou a taxa de juros para 3,75% a.a., e sinalizou espaço para uma pausa na próxima reunião. Destaque também para a leitura preliminar do PIB da Zona do Euro, que cresceu a 0,3% no 2º trimestre, apesar da atividade industrial continuar em retração. Por sua vez, a guerra da Ucrânia segue sem uma definição, com a Rússia anunciando o fim acordo de exportação do Mar Negro em julho, o que deve afetar negativamente a exportação de grãos da Ucrânia.

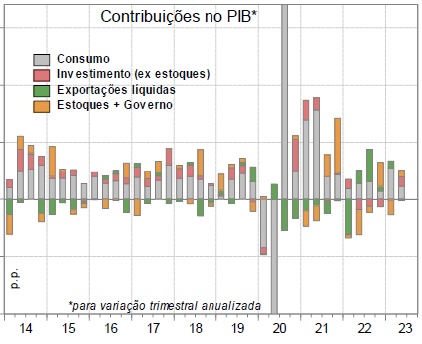

Na China, a atividade continuou em baixa. Este sintoma se refletiu no PIB do segundo trimestre, que expandiu em 6,3% na comparação anual, número abaixo da expectativa do mercado (7,3%) e justificado pela queda das exportações e um consumo mais fraco.

Brasil

O Ibovespa, por sua vez, avançou em 3,3% em um mês marcado por um cenário externo positivo, por novos registros de queda no IPCA, e pela expectativa de corte na taxa Selic, evento este que se concretizou logo no início de agosto, quando o Copom entregou uma queda de 0,50 p.p., levando a taxa a 13,25%.

Em julho, o IPCA-15 atingiu 3,2% em 12 meses. Houve desaceleração dos núcleos, puxada pelos preços livres e pela queda dos preços da alimentação no domicílio. Os preços dos bens industriais caíram 0,6% no mês com auxílio do programa governamental de incentivos para venda de automóveis novos. Até o final do mês, a expectativa de inflação para 2023 era de 4,9% de acordo com o Relatório Focus, pouco acima do limite superior da meta, enquanto para 2024 a expectativa era de 3,9% a.a.

Disclaimer

Wright Capital Gestão de Recursos Ltda. ("Wright Capital") does not market or distribute investment fund shares or any other financial asset. This material is for informational purposes only and is intended exclusively for its recipient. The information contained herein is strictly confidential and may not be used by anyone other than the intended recipient or disclosed to third parties without the prior written consent of Wright Capital. This material does not constitute an official investment statement for the funds or assets referenced herein, which will be prepared and sent by the fund administrator at the appropriate time, where applicable. In the event of any discrepancy between the information contained in this material and that contained in the monthly statement issued by the fund administrator, the information in such monthly statement shall prevail. Discrepancies may arise due to the adoption of different calculation and presentation methods. Net asset values of investment funds that may be contained in this document are net of expenses (i.e. fees, commissions, and taxes). Fund performance figures disclosed in this document are not net of taxes. Investment funds may use derivative strategies as an integral part of their investment policies. Such strategies, as adopted, may result in significant losses for shareholders, potentially exceeding the invested capital and giving rise to an obligation to contribute additional funds to cover such losses. For performance evaluation purposes, a minimum analysis period of 12 (twelve) months is recommended. Multi-market funds with equity exposure and equity funds may be subject to significant concentration in assets of a limited number of issuers, with the risks arising therefrom. Private credit funds are subject to the risk of substantial loss of net assets in the event of non-payment of portfolio assets, including due to intervention, liquidation, administration, bankruptcy, or judicial or extrajudicial reorganization of the issuers. Certain market index comparisons may have been included for reference purposes only and do not represent a return guarantee by Wright Capital. Past results do not guarantee future performance and are not backed by Wright Capital, any of its affiliates, the administrator, any insurance mechanism, or the Credit Guarantee Fund (FGC). Investors are advised to carefully read fund regulations and prospectuses before investing. Investments involve exposure to risks, including the possibility of total loss of the invested amount. This document does not constitute a legal or any other form of opinion or recommendation by Wright Capital and does not take into account the particular circumstances of any individual. The use of the information contained herein is entirely at the user’s own risk. Before making any investment decision, Wright Capital recommends that the interested party consult their own legal advisor.