Macro Report December 2024

Internacional

Em novembro, a eleição de Donald Trump impulsionou as bolsas e valorizou o dólar nos EUA. Em outros mercados, o sentimento foi misto diante da expectativa de uma política comercial mais hostil sob seu governo.

Há expectativa de que Trump adote medidas inflacionárias, seja por tarifas protecionistas, seja por expansionismo fiscal. Essas políticas podem impactar as decisões do FOMC, que, embora deva reduzir os juros em 0,25% em dezembro, pode rever a extensão do ciclo de cortes.

Na Europa, a retração da atividade se agravou, e este quadro, somado a questões fiscais, tem alimentado problemas políticos em alguns países. Na Alemanha, o avanço de partidos populistas levou à antecipação das eleições. Na França, o primeiro-ministro foi deposto após aprovar um orçamento por manobra constitucional. No Reino Unido, há pressão por novas eleições após a primeira-ministra propor um pacote de aumento de impostos e gastos. Esses desafios, combinados com a guerra na Ucrânia e as eleições americanas, continuam a impor grandes obstáculos à economia europeia.

Na China, a economia apresentou melhora marginal nos últimos meses. Em outubro, as vendas no varejo cresceram 4,8%, o maior avanço em oito meses, e a produção industrial subiu 5,3%, superando as expectativas.

A possível retomada de políticas protecionistas nos EUA pode intensificar tensões comerciais com a China, potencialmente resultando em uma guerra comercial. Por outro lado, se outras economias mundiais também se prejudicarem com taxações americanas, elas podem tentar cultivar laços comerciais mais profundos com a China. Assim, deve persistir o esforço do país para estreitar relações com outros parceiros, como vem fazendo com o Brasil.

Brasil

O cenário externo, somado à incerteza fiscal doméstica, desestabilizou o câmbio e a curva de juros no Brasil. A desvalorização cambial dificulta o trabalho do Banco Central, que já enfrenta o desafio de um hiato do produto positivo.

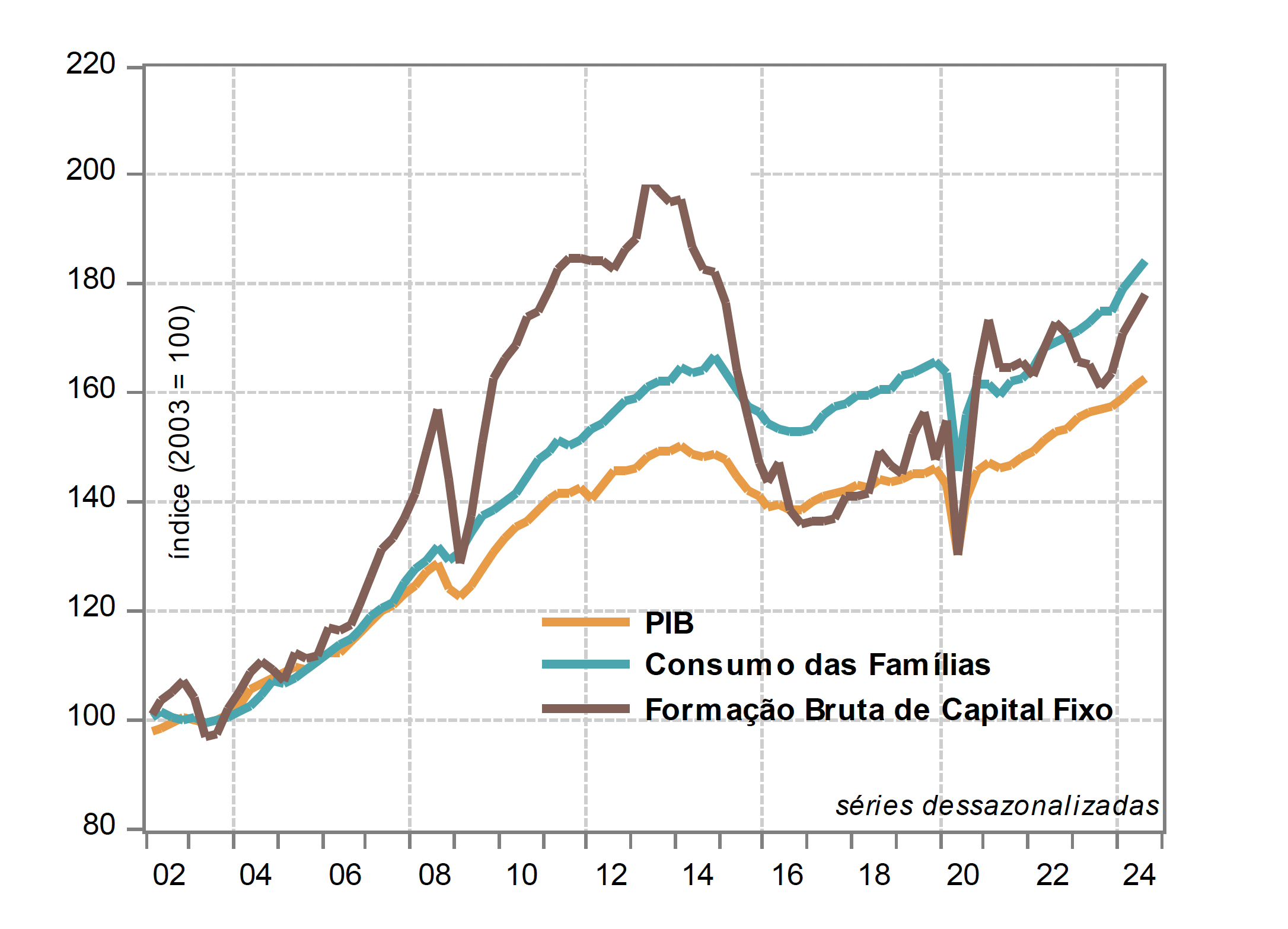

No 3T24, o PIB cresceu 0,9%, impulsionado pelo consumo das famílias e pelos gastos do governo. A taxa de desemprego atingiu o menor nível histórico e deve continuar caindo enquanto o crescimento permanecer acima do potencial.

A persistente desancoragem das expectativas de inflação também reflete a incerteza sobre a condução da política monetária, especialmente com a transição para Galípolo na presidência do BC em janeiro.

O quadro fiscal também piorou após o pacote anunciado pelo governo, que inclui medidas como ajustes no abono salarial, Fundeb e DRU, além de mudanças no salário-mínimo e aposentadoria dos militares. Algumas medidas exigem mudanças constitucionais, enquanto outras dependem de leis complementares. A proposta de limitar o crescimento de emendas parlamentares enfrenta resistência no Congresso.

A isenção do IR para rendas até R$ 5 mil, embora prometendo neutralidade na arrecadação, foi mal-recebida por desviar o foco da redução de gastos e pode pressionar a inflação ao aumentar a renda disponível.

Tudo mais constante, o cenário político e econômico no Brasil deve continuar abalando a confiança dos investidores e o desenvolvimento da economia nacional.

Disclaimer

Wright Capital Gestão de Recursos Ltda. ("Wright Capital") does not market or distribute investment fund shares or any other financial asset. This material is for informational purposes only and is intended exclusively for its recipient. The information contained herein is strictly confidential and may not be used by anyone other than the intended recipient or disclosed to third parties without the prior written consent of Wright Capital. This material does not constitute an official investment statement for the funds or assets referenced herein, which will be prepared and sent by the fund administrator at the appropriate time, where applicable. In the event of any discrepancy between the information contained in this material and that contained in the monthly statement issued by the fund administrator, the information in such monthly statement shall prevail. Discrepancies may arise due to the adoption of different calculation and presentation methods. Net asset values of investment funds that may be contained in this document are net of expenses (i.e. fees, commissions, and taxes). Fund performance figures disclosed in this document are not net of taxes. Investment funds may use derivative strategies as an integral part of their investment policies. Such strategies, as adopted, may result in significant losses for shareholders, potentially exceeding the invested capital and giving rise to an obligation to contribute additional funds to cover such losses. For performance evaluation purposes, a minimum analysis period of 12 (twelve) months is recommended. Multi-market funds with equity exposure and equity funds may be subject to significant concentration in assets of a limited number of issuers, with the risks arising therefrom. Private credit funds are subject to the risk of substantial loss of net assets in the event of non-payment of portfolio assets, including due to intervention, liquidation, administration, bankruptcy, or judicial or extrajudicial reorganization of the issuers. Certain market index comparisons may have been included for reference purposes only and do not represent a return guarantee by Wright Capital. Past results do not guarantee future performance and are not backed by Wright Capital, any of its affiliates, the administrator, any insurance mechanism, or the Credit Guarantee Fund (FGC). Investors are advised to carefully read fund regulations and prospectuses before investing. Investments involve exposure to risks, including the possibility of total loss of the invested amount. This document does not constitute a legal or any other form of opinion or recommendation by Wright Capital and does not take into account the particular circumstances of any individual. The use of the information contained herein is entirely at the user’s own risk. Before making any investment decision, Wright Capital recommends that the interested party consult their own legal advisor.