Macro Report March 2025

Internacional

Nos EUA, as bolsas foram impactadas pela incerteza gerada pela política externa de Donald Trump e seus possíveis efeitos sobre o crescimento econômico americano. Na Europa, os índices apresentaram alta, impulsionados pelas promessas de maior estímulo econômico e aumentos nos gastos com defesa pela Alemanha e pela União Europeia. Já na China, as empresas de tecnologia mantiveram-se em alta, sustentadas pelo otimismo desencadeado em janeiro, após o evento DeepSeek.

No que diz respeito à política externa americana, além das taxações sobre o México e Canadá, que foram adiadas para abril, o governo Trump anunciou a intenção de aplicar tarifas de 25% sobre produtos da União Europeia e 10% sobre os importados chineses, com a perspectiva de adotar tarifas recíprocas a partir de abril. Este cenário fez o mercado precificar um crescimento mais modesto para os EUA a partir de 2025, destacando como possíveis fatores de desaceleração a diminuição da renda disponível e do consumo, condições financeiras mais restritivas e uma queda nos indicadores de confiança, que podem levar a uma redução dos investimentos.

O risco inflacionário também tende a aumentar. O mercado segue projetando cortes nas taxas de juros pelo FOMC a partir de junho de 2025, apesar das recentes declarações de Jerome Powell, que indicam que o Federal Reserve não tem pressa para reduzir os juros, devido ao persistente cenário inflacionário e aos potenciais impactos econômicos das novas políticas comerciais do governo. Em março, apesar de a criação de empregos ter ficado abaixo das expectativas, este dado isolado não foi suficiente para alterar o tom do FOMC para as próximas reuniões.

Do outro lado do Atlântico, as expectativas de crescimento para a Alemanha e a União Europeia aumentaram. As eleições parlamentares alemãs confirmaram a vitória de Friedrich Merz, do partido de centro-direita União Democrata Cristã (CDU), que se comprometeu a aumentar os investimentos em infraestrutura e defesa, rompendo com décadas de austeridade fiscal. Por sua vez, a União Europeia anunciou planos de ampliar os investimentos em defesa, como resposta ao encerramento do suporte financeiro e bélico dos EUA à Ucrânia. Contudo, desafios estruturais persistem para o bloco, como o envelhecimento populacional, a alta dos custos energéticos e os riscos geopolíticos.

Brasil

No Brasil, o impacto da política comercial de Trump provocou uma reprecificação dos ativos, resultando na queda do Ibovespa e na desvalorização do real. A curva de juros apresentou recuo acentuado, à medida que dados de atividade indicam um desaquecimento da economia.

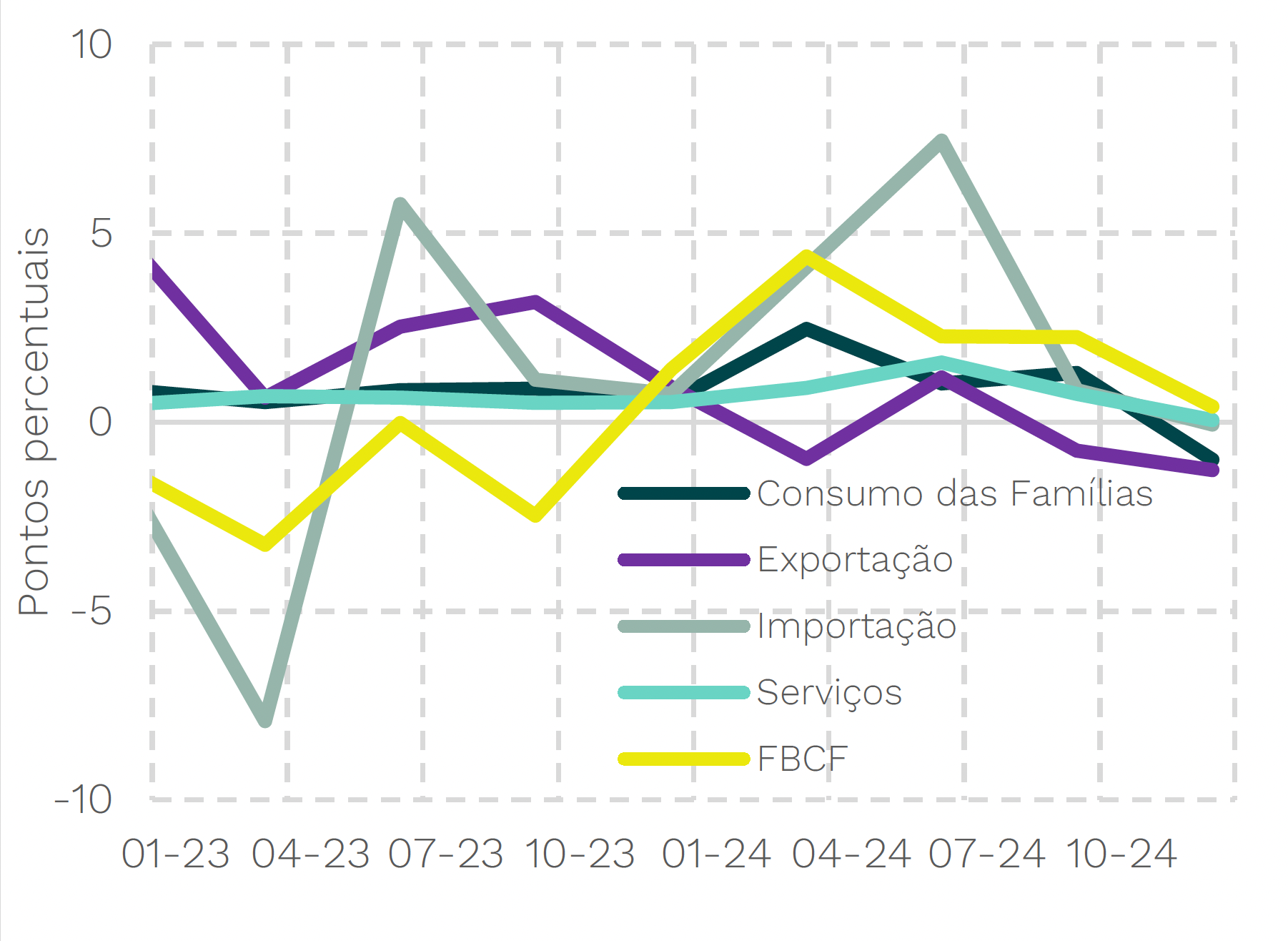

O PIB do 4T24 cresceu 0,2% no trimestre e 3,6% no ano, abaixo das expectativas de mercado, sugerindo uma moderação no ritmo de crescimento, que foi desigual entre os setores. No lado da oferta, as surpresas negativas vieram da agricultura (-2,3%) e dos serviços (0,1%), enquanto a indústria registrou expansão (0,3%). No lado da demanda, o consumo das famílias teve queda de 1,0%, enquanto a formação bruta de capital fixo cresceu 0,4%. As exportações e importações recuaram, com quedas de 1,3% e 0,1%, respectivamente.

Com a elevação dos juros, a expectativa é que o PIB continue a desacelerar em 2025, a partir do segundo semestre. No entanto, uma possível expansão fiscal para mitigar esse movimento poderá influenciar essa tendência.

Disclaimer

Wright Capital Gestão de Recursos Ltda. ("Wright Capital") does not market or distribute investment fund shares or any other financial asset. This material is for informational purposes only and is intended exclusively for its recipient. The information contained herein is strictly confidential and may not be used by anyone other than the intended recipient or disclosed to third parties without the prior written consent of Wright Capital. This material does not constitute an official investment statement for the funds or assets referenced herein, which will be prepared and sent by the fund administrator at the appropriate time, where applicable. In the event of any discrepancy between the information contained in this material and that contained in the monthly statement issued by the fund administrator, the information in such monthly statement shall prevail. Discrepancies may arise due to the adoption of different calculation and presentation methods. Net asset values of investment funds that may be contained in this document are net of expenses (i.e. fees, commissions, and taxes). Fund performance figures disclosed in this document are not net of taxes. Investment funds may use derivative strategies as an integral part of their investment policies. Such strategies, as adopted, may result in significant losses for shareholders, potentially exceeding the invested capital and giving rise to an obligation to contribute additional funds to cover such losses. For performance evaluation purposes, a minimum analysis period of 12 (twelve) months is recommended. Multi-market funds with equity exposure and equity funds may be subject to significant concentration in assets of a limited number of issuers, with the risks arising therefrom. Private credit funds are subject to the risk of substantial loss of net assets in the event of non-payment of portfolio assets, including due to intervention, liquidation, administration, bankruptcy, or judicial or extrajudicial reorganization of the issuers. Certain market index comparisons may have been included for reference purposes only and do not represent a return guarantee by Wright Capital. Past results do not guarantee future performance and are not backed by Wright Capital, any of its affiliates, the administrator, any insurance mechanism, or the Credit Guarantee Fund (FGC). Investors are advised to carefully read fund regulations and prospectuses before investing. Investments involve exposure to risks, including the possibility of total loss of the invested amount. This document does not constitute a legal or any other form of opinion or recommendation by Wright Capital and does not take into account the particular circumstances of any individual. The use of the information contained herein is entirely at the user’s own risk. Before making any investment decision, Wright Capital recommends that the interested party consult their own legal advisor.