Macro Report May 2025

Internacional

O anúncio e posterior recuo na imposição de tarifas comerciais pelos EUA elevou a volatilidade dos mercados em abril, afetando bolsas, câmbio e juros. O ouro atingiu novas máximas, enquanto o petróleo recuou devido ao aumento da oferta pela OPEP e aos temores de desaceleração global.

Com o “Liberation Day” reforçando a percepção de que o comércio com os EUA deve se tornar mais difícil, o mercado passou a revisar para baixo as projeções de crescimento do país, elevando as probabilidades de uma recessão. Como reflexo, com importadores se antecipando ao cenário de tarifas mais altas, o PIB do primeiro trimestre recuou 0,3%. No entanto, essa leitura isolada pode distorcer a real dinâmica da economia, já que o mercado de trabalho segue robusto: a taxa de desemprego permanece abaixo de 4,2%, nível considerado compatível com o pleno emprego segundo o Fed, o que justifica a cautela do banco central antes de qualquer ajuste nos juros.

Na Zona do Euro, o PIB cresceu 0,4% no 1T25, mas o resultado foi inflado por um salto de 3,2% na Irlanda. Sem esse efeito, o crescimento teria ficado entre 0,2% e 0,3%. A confiança na região começa a recuar diante do agravamento da guerra comercial. A recente derrota de Friedrich Merz no parlamento alemão sinaliza desafios políticos adicionais que devem afetar todo o bloco. No campo monetário, o BCE deve manter sua política acomodaticia, sustentada pela valorização do euro, pela queda nos preços de energia e pela menor atividade econômica.

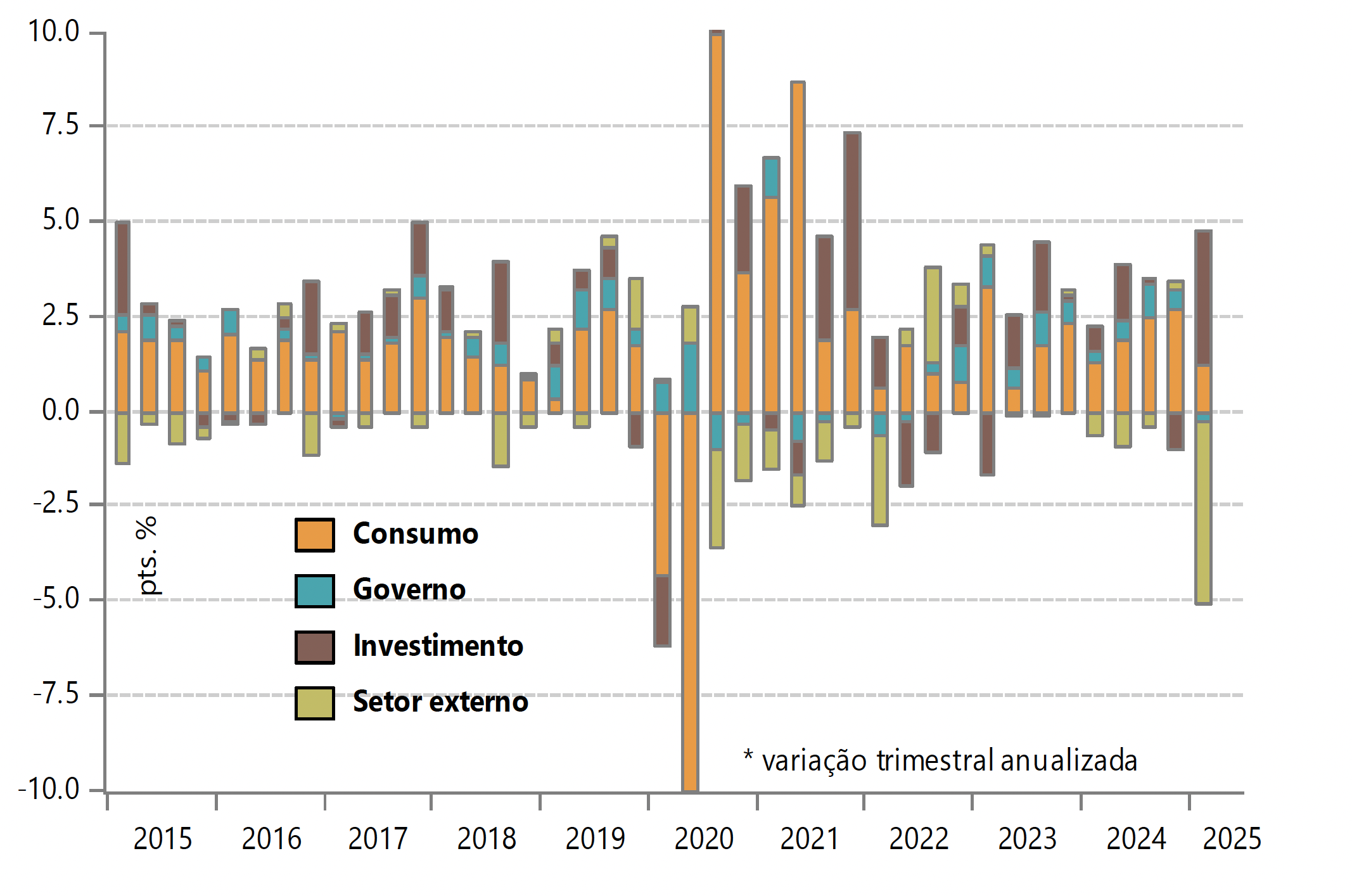

Na China, o PIB cresceu 5,4% no 1T25, impulsionado por exportações antecipadas, maior produção industrial e alta no varejo. No entanto, o agravamento da disputa com os EUA – que já impõem tarifas superiores a 100% – deve afetar o desempenho da economia chinesa no médio prazo. Mesmo assim, os ativos chineses demonstram resiliência: o renminbi se valorizou e os títulos públicos operam em máximas. Em resposta ao cenário, o governo anunciou 23 medidas de estímulo, abrangendo apoio à demanda, às pequenas exportadoras e ao mercado de capitais.

Brasil

No Brasil, o Copom elevou a Selic em 50 bps, para 14,75%, como esperado. O comitê indicou que os riscos seguem equilibrados, mas destacou a necessidade de cautela diante da incerteza e do estágio avançado do ciclo. Uma nova alta, se ocorrer, deve ser menor. O mercado, no entanto, já projeta um corte de 25 bps.

Do ponto de vista da atividade, esta pode se enfraquecer devido à redução das exportações e dos preços das commodities, mas o Brasil pode ganhar espaço no comércio com a China.

Internamente, a economia começou 2025 com o impulso da safra recorde de soja. O desemprego segue estável e o consumo mostra resistência, com impacto sobre o emprego ocorrendo com atraso. Os salários reais subiram 4,5% no 1º trimestre, ampliando a renda das famílias. O governo busca estimular o crédito com novas regras para o consignado privado, mas o alto endividamento exige prudência.

Já a arrecadação federal deve se manter em 2025 e 2026, embora haja riscos relacionados a fontes extraordinárias, à desaceleração da atividade e à queda no petróleo. Nesse contexto, a proposta de isenção do IR aumenta a incerteza fiscal, somando-se à LDO de 2026, que projeta despesas obrigatórias subestimadas e pressiona o espaço para gastos discricionários.

Disclaimer

Wright Capital Gestão de Recursos Ltda. ("Wright Capital") does not market or distribute investment fund shares or any other financial asset. This material is for informational purposes only and is intended exclusively for its recipient. The information contained herein is strictly confidential and may not be used by anyone other than the intended recipient or disclosed to third parties without the prior written consent of Wright Capital. This material does not constitute an official investment statement for the funds or assets referenced herein, which will be prepared and sent by the fund administrator at the appropriate time, where applicable. In the event of any discrepancy between the information contained in this material and that contained in the monthly statement issued by the fund administrator, the information in such monthly statement shall prevail. Discrepancies may arise due to the adoption of different calculation and presentation methods. Net asset values of investment funds that may be contained in this document are net of expenses (i.e. fees, commissions, and taxes). Fund performance figures disclosed in this document are not net of taxes. Investment funds may use derivative strategies as an integral part of their investment policies. Such strategies, as adopted, may result in significant losses for shareholders, potentially exceeding the invested capital and giving rise to an obligation to contribute additional funds to cover such losses. For performance evaluation purposes, a minimum analysis period of 12 (twelve) months is recommended. Multi-market funds with equity exposure and equity funds may be subject to significant concentration in assets of a limited number of issuers, with the risks arising therefrom. Private credit funds are subject to the risk of substantial loss of net assets in the event of non-payment of portfolio assets, including due to intervention, liquidation, administration, bankruptcy, or judicial or extrajudicial reorganization of the issuers. Certain market index comparisons may have been included for reference purposes only and do not represent a return guarantee by Wright Capital. Past results do not guarantee future performance and are not backed by Wright Capital, any of its affiliates, the administrator, any insurance mechanism, or the Credit Guarantee Fund (FGC). Investors are advised to carefully read fund regulations and prospectuses before investing. Investments involve exposure to risks, including the possibility of total loss of the invested amount. This document does not constitute a legal or any other form of opinion or recommendation by Wright Capital and does not take into account the particular circumstances of any individual. The use of the information contained herein is entirely at the user’s own risk. Before making any investment decision, Wright Capital recommends that the interested party consult their own legal advisor.