Macro Report July 2024

Internacional

Nos EUA, índices se valorizam na onda de AI, cenário mais benigno de inflação.

Na reunião de junho, o FOMC manteve a taxa de juros entre 5,25% e 5,50%, e em comunicado demonstrou que permanecerá data driven e com juros altos por mais tempo para assegurar a trajetória de desinflação. As novas projeções disponibilizadas pelo FOMC sustentam esse cenário de juros maiores por mais tempo, com a estimativa para os juros passando para 5,1% no final de 2024 (ante 4,6%) e 4,1% em 2025 (ante 3,9%). Paralelamente, o PCE de maio reforçou um cenário mais benigno para a inflação, caindo de 2,7% para 2,6%. O mercado de trabalho, contudo, continua em alta, e ainda pode exercer pressões inflacionárias adicionais.

No cenário político, o primeiro debate presidencial colocou em dúvida a capacidade de Joe Biden (Partido Democrata) de ganhar a eleição e de governar por mais quatro anos. Tanto na agenda Democrata quanto na Republicana a expansão do plano de isenção fiscal de 2017, o Tax Cuts and Jobs Act, e a trajetória dos déficits seguem sendo temas essenciais.

Na Europa, as votações para o Parlamento Europeu também geraram ruído após o avanço da extrema direita. Em resposta, o presidente francês Emanuel Macron convocou eleições domésticas, levando, contudo, a um esvaziamento da força política da centro-direita no parlamento nacional. Este novo panorama político gera preocupações sobre o populismo e suas consequências fiscais para a UE, dado que países como a própria França já estão fora do limite de déficit do bloco.

Brasil

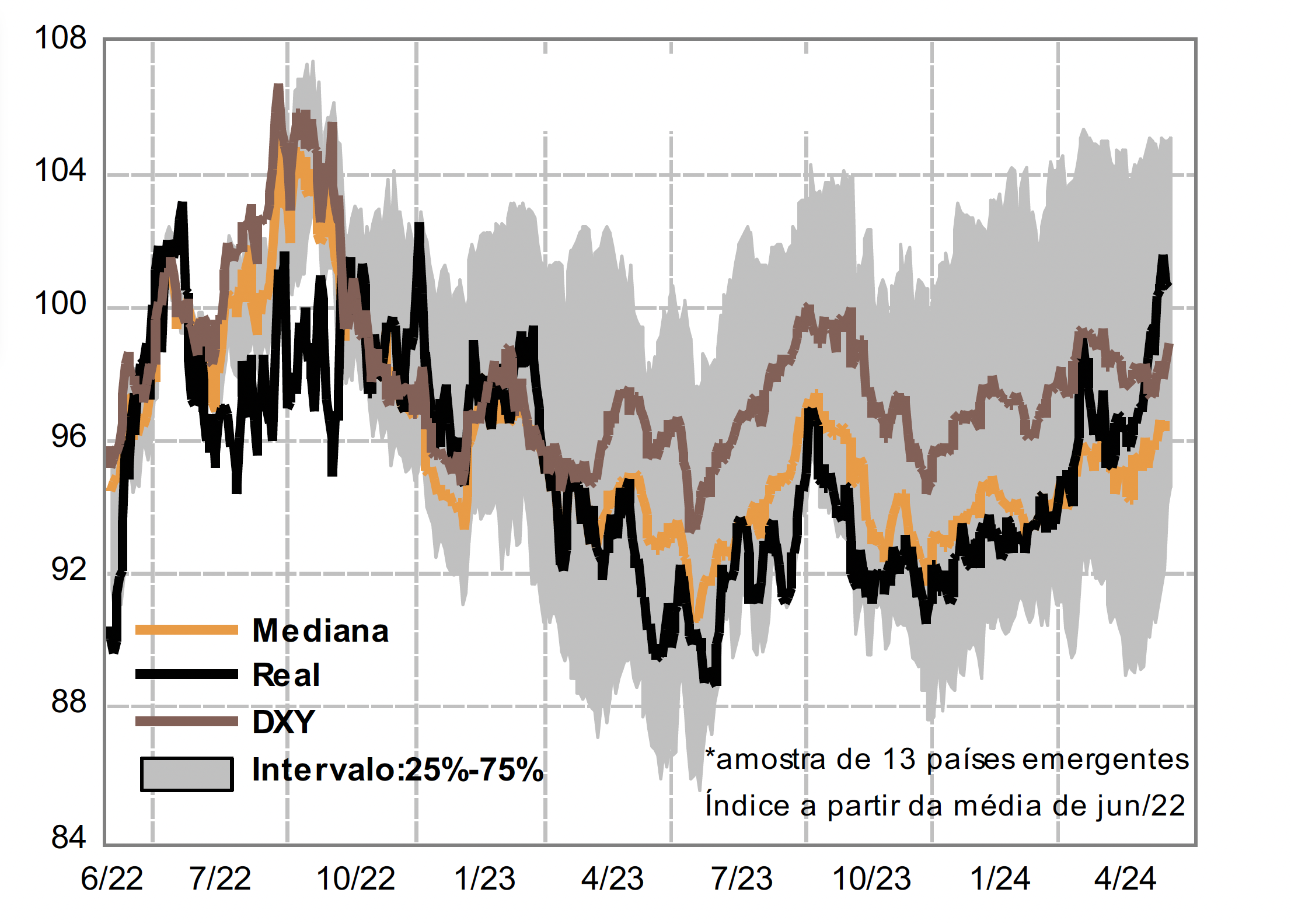

No Brasil, o câmbio e as curvas de juros sofreram com os efeitos dos ataques do Presidente Lula à autoridade monetária, e com as perdas de Fernando Haddad no Congresso.

Em junho o Copom votou em unanimidade pela manutenção da Selic em 10,5%, encerrando o ciclo de cortes. No geral, o contexto monetário segue duro e pautado em uma ampla desancoragem das expectativas de inflação diante da perda de credibilidade fiscal do governo, e da dissidência ocorrida na penúltima reunião do comitê. Além disso, o IPCA parou de dar sinais benignos e o mercado de trabalho segue apertado, com a taxa de desemprego em 7,0%.

De forma a ajustar a política fiscal, o governo continua a insistir na expansão das receitas, apesar das dificuldades em emplacar emendas de arrecadação. As tentativas de Haddad de gerar receitas via desoneração da folha de pagamentos e compensação de créditos PIS/Cofins foram rejeitadas pelos parlamentares, em custosa derrota para sua credibilidade.

Mesmo com a forte arrecadação no início do ano, o déficit primário do setor público chegou a 2,5% em maio (R$ 63,9 bi), maior do que o esperado. O mercado segue cético em relação à questão fiscal, o que tem se verificado na abertura da curva de juros atrelada à inflação, e na desvalorização do real.

O recente choque cambial sobre o real pode ter impactos principalmente sobre a inflação de bens industriais. Isto acontece pela maior concentração de bens de demanda atendidas pelas importações. Com um potencial fim do comportamento benigno deste indicador, e uma inflação de serviços no patamar de 5,0%, é possível um repique do IPCA nos próximos meses.

Disclaimer

Wright Capital Gestão de Recursos Ltda. ("Wright Capital") does not market or distribute investment fund shares or any other financial asset. This material is for informational purposes only and is intended exclusively for its recipient. The information contained herein is strictly confidential and may not be used by anyone other than the intended recipient or disclosed to third parties without the prior written consent of Wright Capital. This material does not constitute an official investment statement for the funds or assets referenced herein, which will be prepared and sent by the fund administrator at the appropriate time, where applicable. In the event of any discrepancy between the information contained in this material and that contained in the monthly statement issued by the fund administrator, the information in such monthly statement shall prevail. Discrepancies may arise due to the adoption of different calculation and presentation methods. Net asset values of investment funds that may be contained in this document are net of expenses (i.e. fees, commissions, and taxes). Fund performance figures disclosed in this document are not net of taxes. Investment funds may use derivative strategies as an integral part of their investment policies. Such strategies, as adopted, may result in significant losses for shareholders, potentially exceeding the invested capital and giving rise to an obligation to contribute additional funds to cover such losses. For performance evaluation purposes, a minimum analysis period of 12 (twelve) months is recommended. Multi-market funds with equity exposure and equity funds may be subject to significant concentration in assets of a limited number of issuers, with the risks arising therefrom. Private credit funds are subject to the risk of substantial loss of net assets in the event of non-payment of portfolio assets, including due to intervention, liquidation, administration, bankruptcy, or judicial or extrajudicial reorganization of the issuers. Certain market index comparisons may have been included for reference purposes only and do not represent a return guarantee by Wright Capital. Past results do not guarantee future performance and are not backed by Wright Capital, any of its affiliates, the administrator, any insurance mechanism, or the Credit Guarantee Fund (FGC). Investors are advised to carefully read fund regulations and prospectuses before investing. Investments involve exposure to risks, including the possibility of total loss of the invested amount. This document does not constitute a legal or any other form of opinion or recommendation by Wright Capital and does not take into account the particular circumstances of any individual. The use of the information contained herein is entirely at the user’s own risk. Before making any investment decision, Wright Capital recommends that the interested party consult their own legal advisor.